As more shoppers go online, the country’s retail landscape is changing rapidly. Traditional brick-and-mortar retailers are facing stiffer competition amid the country’s digital transformation, leading to falling sales and shares of total retail business (although far from outright death). Meanwhile, e-commerce retailers like Amazon continue to expand the scale and reach of their operations. Nationally, the economic effects are widespread, particularly when it comes to the labor market: E-commerce is hiring, while certain brick-and-mortar retailers are shedding jobs.

As the brick-to-bits transition continues, it’s not enough to just count job and output changes. It’s equally important to know wheree-commerce jobs are emerging, especially as it relates to more traditional retail locations. This matters for at least a few reasons:

- Workers’ access to jobs matters for both employees and employers. Job sprawl is associated with longer commutes, makes transit less convenient, and can make it more difficult for companies to find qualified workers. If e-commerce jobs are harder to reach than the retail jobs they replace, it could create a drag on regional economic growth.

- Local fiscal impacts will vary depending on where establishments are gained and lost. Retail and e-commerce establishments generate significant local tax revenue, but also demand public services like physical infrastructure. These dynamics may create winners and losers among local governments.

- Warehousing and traditional retail generate different transportation patterns. Brick-and-mortar retail relies on small supply deliveries, using large parking lots to help customers carry goods the last mile(s) home. E-commerce warehouses, by contrast, generate more local delivery trips right to people’s doors, use large trucks to stock the warehouse, and generally need less parking. In each case, localities must ensure local roads and parking can handle the associated traffic.

By looking at where e-commerce and other brick-and-mortar employers concentrate their facilities—or “establishments” in statistical parlance—we can begin to explore these issues in greater depth. In particular, we use Census Zip Business Patterns to more precisely analyze where these establishments have grown or declined between 2012 and 2016, including their size, count, and geographic reach across different metro areas.

For the purposes of this analysis, we define e-commerce industries as those involved in electronic shopping (which includes the offices for online retail establishments like Walmart and Amazon) and warehousing (which includes warehouses of major logistics companies like DHL and warehouses owned by Amazon). In addition, we look at all types of establishment sizes in these industries, bundling establishments as small (1 to 49 employees), medium (50 to 249 employees), and large (250 employees or more).

This analysis reveals four notable trends:

1. THE NUMBER OF E-COMMERCE ESTABLISHMENTS IS GROWING QUICKLY AND ACROSS ALL ESTABLISHMENT SIZES

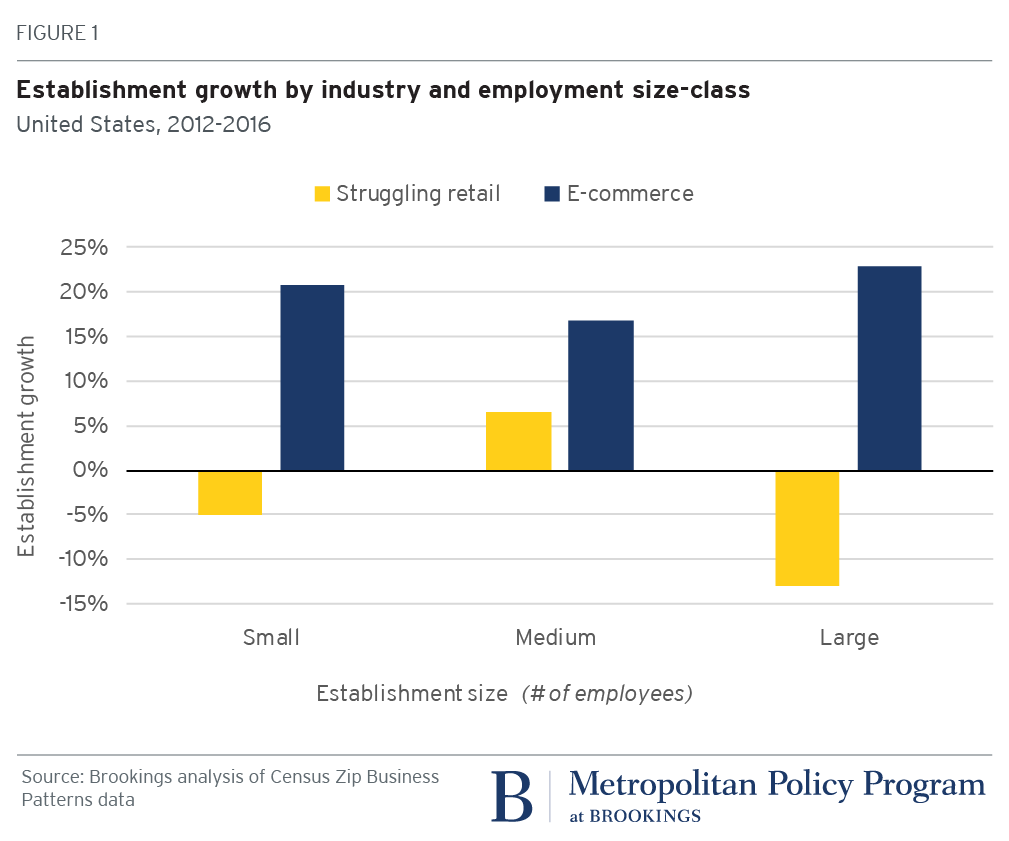

Not surprisingly, as e-commerce drives more sales and employment growth nationally, the number of related establishments has also climbed. Looking at national numbers from 2012 to 2016—where consistent industry data exist—e-commerce industries grew by 8,269 establishments, or 20.6 percent. This was far faster than the national average of 4.4 percent across all industries.

By contrast, the four industries we categorize as struggling brick-and-mortar retailers—clothing stores; book stores and news dealers; department stores; and office supplies, stationery, and gift stores—saw a decline in their total establishment count over the same time period. Establishments in these four industries were down by 4.2 percent, which amounted to a net loss of 6,120 establishments nationally.

Critically, e-commerce isn’t just growing in the aggregate. Establishments of all sizes experienced growth over the four-year period (Figure 1). Startup activity looked strong, as indicated by the 23.4 percent jump in small electronic shopping establishments. The number of large warehouses continued to grow too, seeing a 20.6 percent gain.

The growth in medium and large e-commerce establishments is especially important because those places of businesses employ much larger shares of total e-commerce employment than the retail industries that are disappearing. In 2016, 62.6 percent of electronic shopping employees and 86.3 percent of warehouse employees worked in medium or large establishments. As a result, the geography of these establishments matters considerably for getting people to work, for moving goods, and for the source of local tax revenue.

2. E-COMMERCE ESTABLISHMENTS SPRAWL MUCH LIKE TRADITIONAL BRICK-AND-MORTAR RETAILERS

As noted above, where e-commerce jobs are located indicates the potential barriers workers may face in trying to access them, especially in suburbs and exurbs. Job sprawl is a national phenomenon, one we’ve studied for years within the country’s 100 largest metropolitan areas.

Similar to struggling brick-and-mortar retailers, we find that emerging e-commerce employers are also sprawling in those same 100 places, based on the distance of these establishments from central business districts (CBDs). For example, 49.9 percent of the country’s struggling brick-and-mortar retailers are located at least 10 miles from a central business district, partly reflecting where their suburban customer base lives (Figure 2). E-commerce actually sprawls a bit more, with 55.9 percent of establishments located more than 10 miles from a CBD, although the electronic shopping and warehousing industries do vary a bit.

E-commerce establishments of all employment sizes grew in all parts of metropolitan areas from 2012 to 2016 (Table 1). Regardless of their distance from a CBD, e-commerce establishments are popping up everywhere. However, with the majority of e-commerce employees working in medium and large establishments, geographic change among those businesses is especially important.

Medium-sized electronic shopping and warehousing establishments are urbanizing the fastest. These kinds of locations within five miles of a CBD can best support transit and other driving alternatives for workers, an advantage that Amazon made notable through its HQ2 search. For warehousing in particular, the jump in central city locations could portend a new kind of warehouse built for modern consumer shopping habits: quicker deliveries, smaller inventories, and reduced parking needs.

Meanwhile, large e-commerce establishments continue to push outward. For warehousing, this reflects how the largest establishments demand significant amounts of land and require strong interstate and local freight access. The largest electronic shopping establishments also tend to locate in places with easier driving, ample parking, and cheaper land. It’s often more difficult for workers to connect to these outlying jobs via transit, causing some peers in the digital economy to run private transportation services.

3. ELECTRONIC SHOPPING ESTABLISHMENTS ARE MORE LIKELY TO LOCATE IN HIGH DENSITY ZIP CODES THAN WAREHOUSES

While both e-commerce industries do tend to sprawl, electronic shopping is far more likely than warehouses to locate within dense job centers—even in the suburbs. (We consider a zip code dense if it’s in the top quartile of jobs per square mile for all U.S. zip codes, which equates to 1,026 jobs per square mile.)

Medium and large electronic shopping establishments more often locate in job-dense areas. This is especially noteworthy at least 10 miles outside of downtowns, where communities typically exhibit low job and housing density. Even here, over 60 percent of electronic shopping establishments are in dense zip codes. Conversely, warehouses are more likely to be found in lower job density locations, even many that are within five miles of the CBD.

As the e-commerce era continues to unfold, these trends suggest we could see more warehouses locating in denser urban centers alongside or in place of brick-and-mortar retail. The increasing frequency and count of parcel deliveries could create motivation on its own. For example, it’s easy to imagine grocery stores transforming retail and storage space to accommodate online shopping habits, something Whole Foods and Walmart are already exploring.

4. E-COMMERCE SPRAWL VARIES ACROSS METRO AREAS

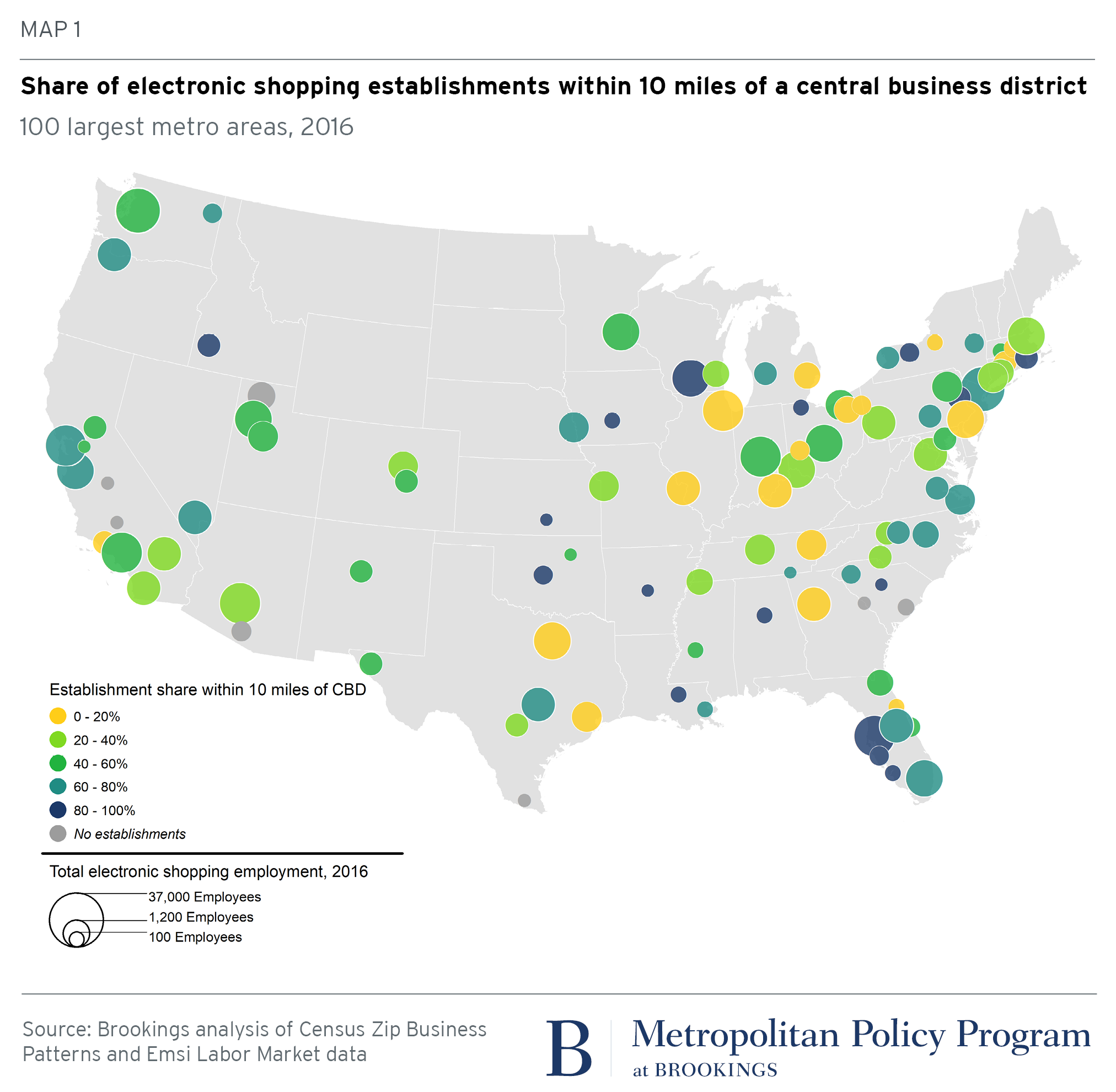

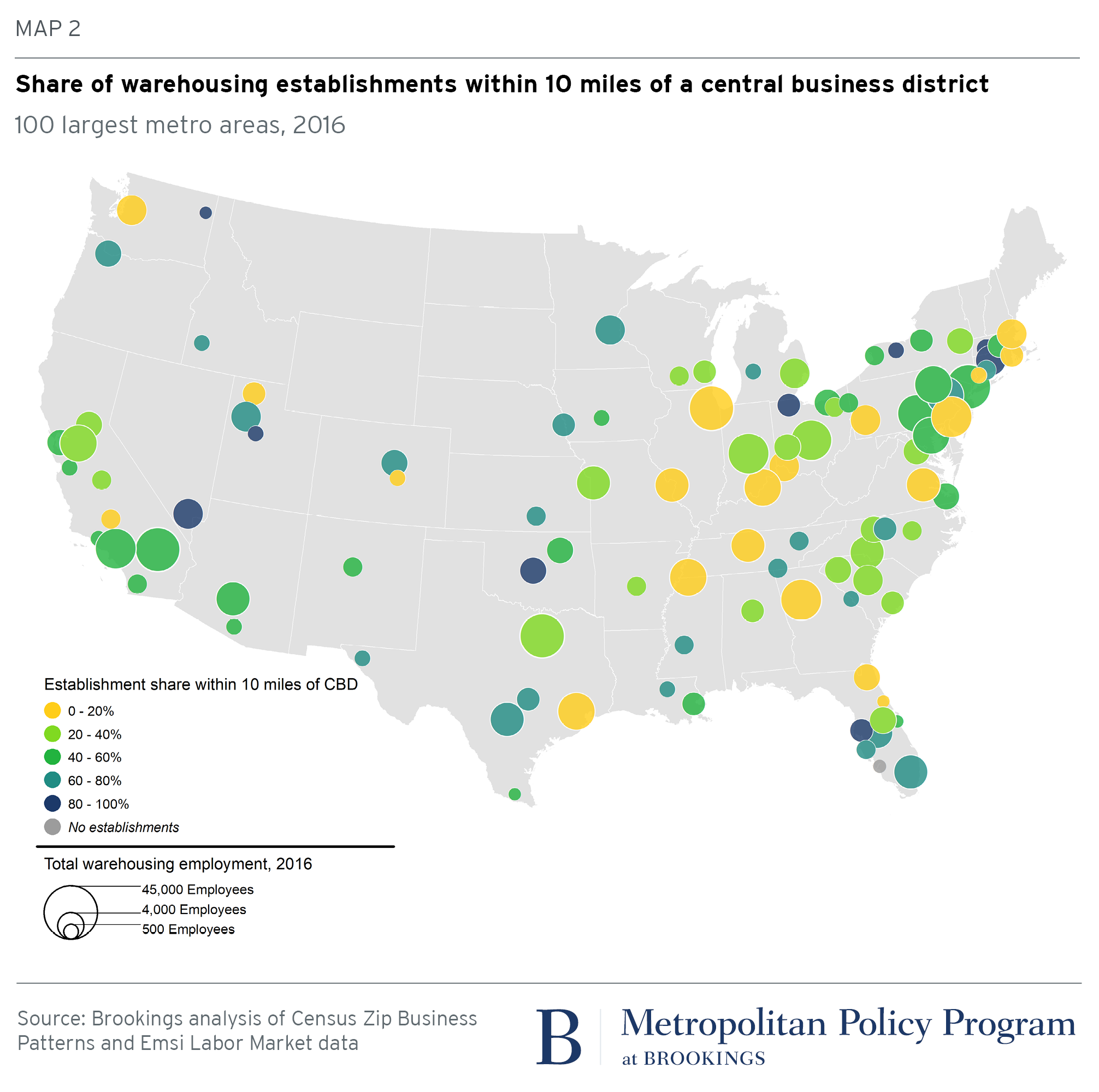

Much like the retail it’s replacing, e-commerce tends to sprawl from metropolitan CBDs. However, this doesn’t mean a suburban and exurban pattern hold in every place. Considering how the majority of employment work in medium and large establishments, mapping where those establishments locate within metro areas reveal considerable variation across the country. The following maps look at the share of medium and large establishments within 10 miles of their metro area’s CBDs, with the circle sizes indicating the total employees in the given industry.

Consider electronic shopping first. As expected, the major coastal tech hubs—San Francisco, San Jose, and New York, for example—have above average shares of these establishments near their CBDs. Tampa, Fla. and Madison, Wis. are also home to large numbers of electronic shopping establishments and large shares near their urban cores, but relatively small electronic shopping markets like Boise City, Idaho; Columbia, S.C.; and Des Moines, Iowa fit the same dense pattern. By contrast, Atlanta, Dallas, and most Ohio metro areas see their electronic shopping establishments sprawl far from their business core.

Warehouses similarly vary in their location within metro areas. Chicago is the second biggest warehousing market after Riverside, Calif., and over 91 percent of medium and large establishments are at least 10 miles from the region’s CBD. Other warehousing hubs like Philadelphia, Memphis, and Louisville display similar patterns. By contrast, in smaller but still sizable warehousing markets like Miami, Minneapolis, and San Antonio, more of these larger warehouses locate near the urban core.

LOCAL POLICYMAKERS MUST PAY CLOSE ATTENTION TO E-COMMERCE’S IMPACTS ON THEIR LOCAL JOB GEOGRAPHY

E-commerce trends related to growth, sprawl, and concentration in job-dense locations reveal a rapidly evolving segment of the economy whose spatial impacts are still in flux. The shift to e-commerce doesn’t portend a sprawl apocalypse or rapid densification for the entire country. Instead, each metro area must confront a wide range of spatial impacts based on its own unique mix of consumer retail demand, industrial specialization, real estate pricing, and land use regimes.

These changes warrant continued attention and analysis. The retail industry is often the largest sector by employment in metro areas, which means local transportation networks, and even housing, are already aligned to connect workers and shoppers to current establishment locations. Similarly, many communities count on the revenues (sales tax, business tax, property tax) from traditional retail. Depending on where e-commerce locates and traditional retailers close, localities could face radically different real estate and fiscal challenges.

The retail industry is often the largest sector by employment in metro areas, which means local transportation networks, and even housing, are already aligned to connect workers and shoppers to current establishment locations.

Going forward, economic development, transportation, and land use policymakers will need to ask challenging questions to manage this level of change. For example:

- Does our market host retail industries that are likely to leave? If they do, are we prepared to replace their fiscal revenues?

- Can we attract both local- and national-serving e-commerce industries? Which are already in our region, where do they tend to locate, and do their jobs offer pathways to prosperity?

- What transportation reforms—capital investments or operational changes—do we need to consider to accommodate these trends?

If e-commerce is the symbol of retail repositioning itself for the digital century, then answering these questions is one way for policymakers to keep pace.

The authors thank Ranjitha Shivaram and Annibel Rice for research assistance on this piece.

This article was originally published in: https://www.brookings.edu